nothing to lose

more thoughts.

The first rate cutting cycle for the Federal Reserve in almost 5 years will most likely begin tomorrow. This got me thinking of course and led me down some rabbit holes. Keep reading if you care to walk through those with me. Hopefully, this makes sense and flows nicely because I feel like I’m going to be jumping around a lot. But also if it doesn’t, I don’t really care lmao. You know the rules. Just clearing my thoughts out in the public.

As always, I appreciate all the kind words from those of you that read these ramblings. Please feel free to to tell me why all of this is the most ridiculous thing you’ve ever read. All feedback helps me to re-evaluate my priors. So in reality, I am actually just using all of you. Cheers.

Just found out they took this whole album off all DSPs and I’m gutted. Thank God for SoundCloud.

rational irrationality

I’ve admitted before that my framing for how I view the the world is economic in nature. Because economics to me is really just about understanding incentives. Knowing the incentive structure of every actor in this “game” of life should, in theory, grant you the ability to make better decisions relative to the person who doesn’t as you can properly assume their best course of action given the options presented to them. We can assume that people will always act in their best self-interest and that most behavior (be it individual, institutional, even cultural) can be explained by what people gain or lose in a given setup. So even if this is an oversimplification, I feel as though it gets me thinking in the right direction for most matters about 80% of the time. For that reason, I won’t stop.

wealth gap = incentive alignment gauge

so, ⬆️ wealth gap → ⬇️ incentive alignment

That leads me to the wealth gap. I’ve been pretty obsessed with wealth inequality these days. And I think the reason as to why I’ve been so consumed by it is that I subconsciously view the wealth gap as a proxy for incentive alignment. And the bigger the gap, the less aligned those games are. When incentives are misaligned whole entire “system” (read as: economy) is threatened by people making sub-optimal choices to bring them back to a position where they can make an optimal choice again. So the wealth gap is really about how badly the game itself is miscalibrated.

⬆️ wealth gap → ⬇️ incentive alignment → ⬆️ sub-optimal choice

where a sub-optimal choice = a risk

So a sub-optimal choice is really just a risk. The increased wealth gap explains why you have to take a risk just to get back to a level playing field. This is why people take on debt for more education because wages stagnated even though they don’t have the cash flow now to pay it back. And why (if you don’t prefer to be a law-abiding citizen), people engage in crime or fraud, since the “normal” options don’t yield enough. I never really understood why I thought about this so much until just now.

⬆️ wealth gap → ⬇️ incentive alignment → ⬆️ rational risk-taking

because a sub-optimal choice or risk =/= irrationality

But people shouldn’t confuse risk-taking with being irrational. I think this is what frustrates me about the boomers who chastize us. Or really just anyone that fundamentally misunderstands the way I think may be so backwards to them lmao. I don’t fault them too much though, because they grew up in a world where the baseline path still worked, so risk looked irrational. In our world, it’s inverted. So we have no choice but to think backwards. When incentives are misaligned, risk-taking is the only rational move left. As the wealth gap widens, the traditional “safe” paths to mobility like steady wages, disciplined saving, and slow asset accumulation stop working. Playing it safe in that environment is actually the irrational choice, because it guarantees stagnation or decline. By contrast, riskier moves — whether that means taking on debt for education, speculating in assets, starting a business, or hustling in the informal economy offer asymmetrically higher payoffs relative to the failing baseline. Even if the odds are low, the expected value of risk beats the certainty of falling behind. In this sense, rising inequality creates a rational shift toward risk at the individual level.

FIRE

⬆️ wealth gap → ⬇️ incentive alignment → ⬆️ rational risk-taking → FIRE movement

An interesting case study of this framework is the FIRE movement. On the surface, FIRE (Financial Independence, Retire Early) looks like a lifestyle trend about extreme saving and early retirement. But through the lens of incentive alignment, it’s really a rational response to a broken system. The traditional baseline path (work hard in a corporate job, climb the ladder, save gradually, retire at 65) no longer produces mobility, stability, or any sense of purpose. The wealth gap ensures that wages don’t keep up, and the work itself often feels extractive and meaningless. So FIRE functions as a rational risk-taking strategy: people aggressively cut expenses and hoard capital as a way to escape from a system where the safe option (staying in corporate work) becomes the irrational decision. If your job delivers little value or purpose and still fails to secure your financial future, then why keep doing something meaningless in the hope it pays off when, if it doesn’t, you might as well have done nothing at all? This is their core argument. In that sense, FIRE shows how misaligned incentives push individuals toward riskier, unconventional choices that are rational at the micro level, even if they reveal systemic dysfunction at the macro level.

the great displacement

I already wrote about how I think AI makes the search for meaning in work a real problem. And the reason why I’m bringing it up again is because it’s all but certain that we’re getting rate cuts from the FOMC on Wednesday. From the last piece:

recall: Fed lowers rates → Bank funding costs decrease → Banks offer cheaper loans → Credit demand increases → New loans create deposits → Money supply expands

The classic assumption is that rate cuts lower financing costs, boost liquidity, and lead to broad-based investment and hiring. That will happen to a degree, but I don’t think the benefits will be evenly distributed. If anything, the dynamic I’ve been outlining about rational risk-taking will show up here too. In a world where inflation runs hotter and the Fed implicitly shifts into a higher inflation-targeting regime, the hurdle rate for capital gets higher. Banks and investors are only going to fund projects that have the potential to beat inflation-adjusted returns. That pushes capital toward riskier, more speculative bets; AI being the clearest example. From the system’s perspective, it looks like irrational exuberance or bubble behavior. But it’s actually completely rational. Why bother financing low-yield, safe projects when the baseline path guarantees negative real returns? Just like with households navigating misaligned incentives, investors will have to adapt by seeking asymmetry. The result is the same paradox: rational choices at the individual level create instability at the macro level, this time in the form of capital misallocation and bubble dynamics. So the Fed thinks it’s just lowering rates, but what it’s really doing is accelerating this regime shift toward risk, creation, and speculation.

⬆️ higher inflation premium + ⬇️ bank funding costs → ⬆️ speculative bets → ⬆️AI investment → ⬆️ displacement of work → ⬇️ sense of meaning/purpose → ⬆️ rational risk-taking

or more simply: ⬆️ higher inflation premium + ⬇️ bank funding costs → ⬆️ rational risk-taking

Half of all US real GDP growth now comes from tech and AI capital expenditure, and that share will only grow as the cost of capital falls and financing becomes easier when the FOMC begins to cut interest rates. This concentration highlights a deeper problem. Most people can no longer define themselves by the work they do, because conventional jobs contribute little to meaningful value creation as we’ve seen by way of the FIRE movement. And like I showed above, I think that their response is very rational in a system where the baseline path offers stagnation at best. The acceleration of AI-driven capital spend only magnifies this dynamic, shrinking opportunities for purposeful work even further and making the incentives for opting out more urgent and rational. In both cases, whether households pursuing FIRE or investors chasing AI returns, rational risk-taking emerges as a response to a system whose incentives are increasingly misaligned. From an earlier piece:

Think about how most people define themselves: by what they do, their job title, their degrees, the status that comes with their education and achievements. It’s how we organize identity and social standing. But what happens when none of that matters anymore? When AI or automation can do the job better, faster, cheaper, and the traditional markers of success lose their value? Suddenly, the credentials that once gave someone purpose and pride feel really pointless. The work that shaped daily routines, social circles, and self-worth disappears. People will be forced to confront the hard question: who am I if not what I do? That kind of identity crisis challenges the core of how we see ourselves and relate to the world.

People are going to have to find the answers to these a lot more quickly than they had intended. That’s if they even thought to ask themselves this at all.

create or speculate

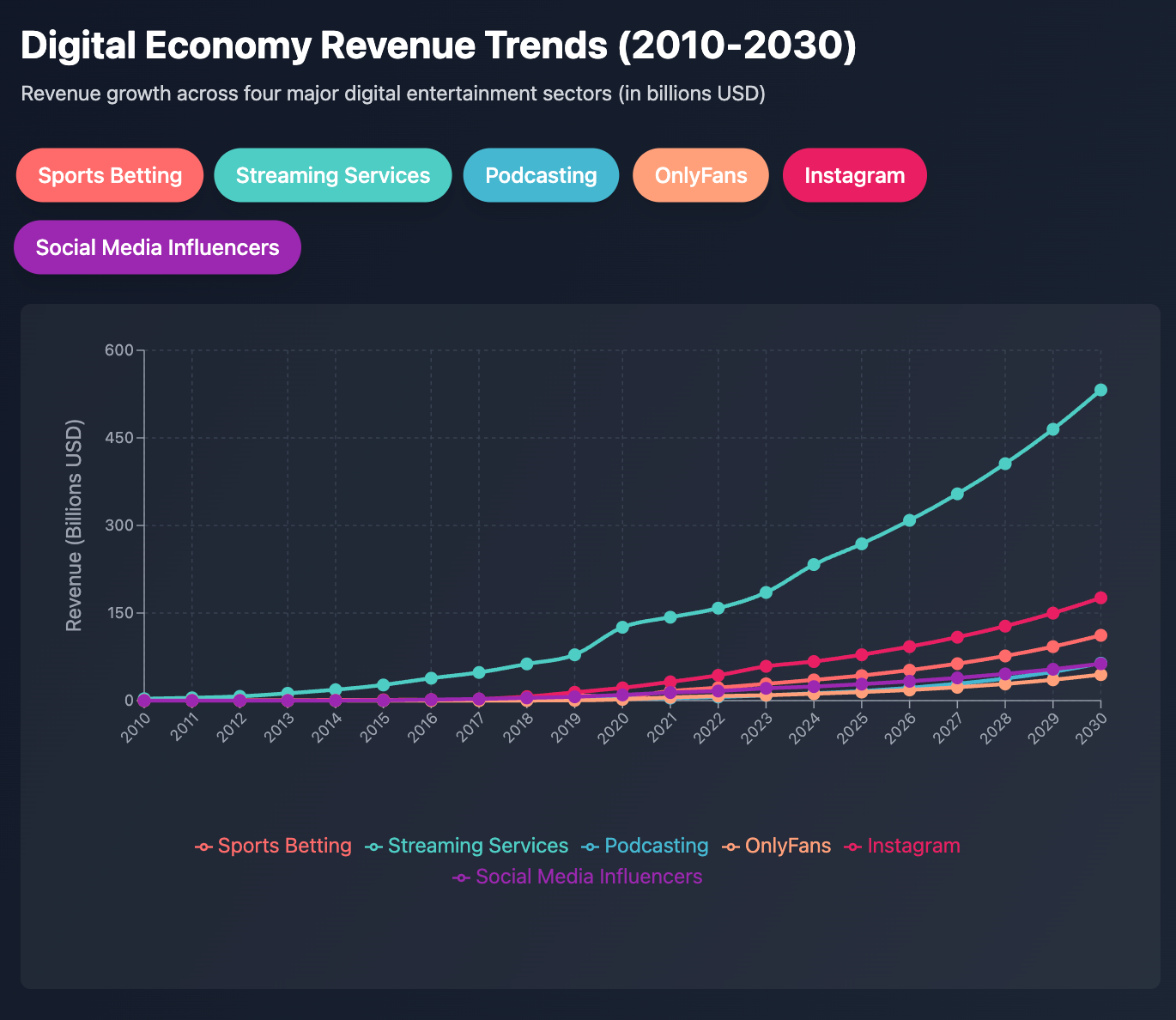

As AI and automation concentrate wealth and value, most conventional work loses both purpose and status as the average worker gets displaced. People are left with a choice: create or speculate. Platforms like OnlyFans, YouTube, Twitch, podcasts, and blogs let you invest your time, creativity, and attention to make money. The upside can be transformative, while the downside is usually just the hours you put in. Seems like a no-brainer to me.

Speculative bets in crypto, meme stocks, SPACs, sports betting, or prediction markets like Polymarket are just different expressions of the same logic. The underlying calculus is the same: when conventional paths fail, taking asymmetric risks is the only rational choice. Creators hedge against purposeless work, speculators hedge against declining real returns or stagnant markets, and bettors hedge against the uncertainty and stagnation of conventional life. Platforms like Polymarket, now approved for U.S. users, and sports betting make it easy to bet on real-world events for the potentially outsized return.

⬆️ AI displacement → ⬇️ meaningful work → ⬆️ rational risk-taking → ⬆️ content creation / speculative economy

Implications: This is all set to accelerate. With the Fed lowering rates and the cost of capital coming down, AI-heavy, capital-intensive projects will get even more funding. That will concentrate wealth further, push conventional work closer to meaninglessness, and force even more people to choose between creating or speculating. At the end of the day, it is all the same person, forced by circumstances to pick a path, to bucket themselves into one of these strategies to reclaim autonomy and upside. These trends will only intensify.

clown show

I worry specifically about the attention economy that’s soon to explode. And specifically streaming. It is the lowest barrier-to-entry industry we have and it’s also growing the fastest.

⬆️ AI displacement → ⬇️ meaningful work → ⬆️ rational risk-taking → ⬆️ content creation → ⬆️ sensationalism/extreme behavior

The problem is that attention is finite. If everyone is participating in this economy, the competition for eyes, clicks, and engagement will only get more intense. As more people chase attention as a scarce resource, the baseline for success keeps rising, forcing individuals to take bigger, riskier, and often more extreme actions just to stand out. Viral stunts, and edgy content is the rational response to a system where the upside of attention is asymmetrical. A single viral moment can transform your social and financial position so you’re incentivized to get it by any means necessary. This dynamic creates a feedback loop where the more people succeed through attention-grabbing moves, the more others are compelled to push the boundaries to compete. What starts as normal content escalates into attention theater, and what seems absurd from the outside is just an inevitable outcome of rational incentives. Everyone is chasing the same finite resource, and the environment rewards risk-takers who can navigate it best, even if their methods of getting it is ridiculous.

the middle man

⬆️ AI displacement → ⬇️ meaningful work → ⬆️ rational risk-taking → ⬆️ creators entering platform economy → ⬆️ middleman rent extraction

This is a layered misalignment. At the same time the baseline employment path fails to provide returns, the alternative path, creation, is not fully liberating either. People are taking on risk to regain autonomy and upside, but a significant portion of that upside is siphoned off by intermediaries. There is an unrealized opportunity for better take rates or ownership structures. If creators are doing the work, building the audience, and supplying the value, why should the platform capture a disproportionate share? There is a strong case, both from efficiency and fairness, for models where creators capture more of the upside. Web3 models, decentralized platforms, or direct subscriber-based approaches like Substack or Paragraph attempt to fix this, but adoption is fragmented and crypto-native audiences remain niche.

So misaligned incentives at the macro level push people into high-risk creation, but misaligned incentives at the platform level siphon the reward from the very people trying to reclaim upside. Solving this will be extremely lucrative.

conclusion

Misaligned incentives are driving rational risk-taking across households, investors, and creators. Cheap capital fuels AI and speculative investment, displacing conventional work and pushing people toward creation or high-variance bets. Platforms take a cut, attention is scarce, and risk escalates, but within that dysfunction lies opportunity.

I wrote all this because I’m thinking about how best to position my capital for this new regime. Big day tmrw. Good luck.